Economic crises are often explained through simple narratives.

“It was caused by tax cuts.”

“It was caused by one government.”

“It could have been avoided with one decision.”

But reality is rarely that simple.

This four-part data series examines Sri Lanka’s foreign exchange crisis through evidence—breaking down what happened, when it happened, and why it unfolded the way it did.

Each story isolates one key question and answers it using data.

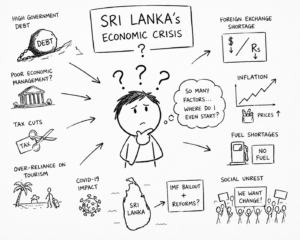

The Core Idea

Sri Lanka’s crisis was not caused by a single event or policy decision.

It was the result of:

- Pre-existing structural weaknesses

- A sudden external shock

- Severe policy constraints during a global crisis

- And decisions made under pressure

The Series

Story #1 — Was the Crisis Already Inevitable by 2019?

Key insight: The economy entered 2020 already vulnerable.

- Growth had slowed to contraction

- Debt had increased sharply

- External exposure had deepened

- Reserves had not improved—despite heavy borrowing

The country had limited buffers to absorb shocks

Conclusion: The crisis did not begin in 2020—it was set up before it.

Story #2 — What Actually Broke the Foreign Exchange System?

Key insight: The system broke when inflows collapsed.

- Tourism earnings fell by over 85%

- FDI declined sharply

- Sri Lanka lost USD 6.5 billion in non-debt inflows (2020–2021)

These are the dollars the country earns—not borrows

Conclusion: The crisis was triggered by a sudden collapse in foreign exchange inflows.

Story #3 — Could Sri Lanka Have Avoided the Crisis by Defaulting Earlier?

Key insight: Policy choices were constrained during the pandemic.

- The country needed foreign exchange for:

- Vaccines and healthcare

- Fuel and food imports

- Defaulting may have preserved reserves—but risked:

- Disrupting financing

- Affecting supply chains

There was no cost-free option.

Conclusion: Decisions were made under extreme constraints, not in normal conditions.

Story #4 — What Changed After the 2022 Debt Standstill?

Key insight: The standstill shifted the crisis into a new phase.

- External financing became more constrained

- Infrastructure projects were delayed

- Costs increased and recovery slowed

Relief in one area created pressure in others.

Conclusion: The standstill did not resolve the crisis—it changed its nature.

Putting It All Together

The crisis unfolded in a sequence:

- Structural Weakness (Pre-2020)

- Rising debt

- Weak reserves

- External vulnerability

- External Shock (2020–2021)

- Collapse of tourism and FDI

- Loss of USD 6.5 billion in inflows

- Policy Constraints

- Pandemic response required foreign exchange

- Limited room for maneuver

- Crisis Transition (2022 onward)

- Debt standstill

- Financing disruptions

- Recovery under tighter conditions

What This Means for Policy

The key lesson is not about assigning blame—it is about understanding systems.

Economic crises are cumulative.

They emerge from:

- Long-term vulnerabilities

- External shocks

- And constrained policy choices

The Bottom Line

Sri Lanka’s foreign exchange crisis was not caused by:

- One policy

- One decision

- Or one government

It was the result of:

A fragile system meeting a severe shock—with limited buffers and difficult trade-offs.

How to Read This Series

- Each story can be read independently

- Together, they provide a complete narrative arc

- The aim is to:

- Clarify complex issues

- Dispel misinformation

- Ground debate in data

Final Note

This series is not about defending or criticizing any single policy position.

It is about: Understanding how economic systems behave under stress—and what the data actually shows.